Future Finance loans and the alternatives

When funds get tight, you won't be alone in feeling tempted by a private student loan. But, there are a lot of factors to consider before taking one out, including the lower-risk alternatives.

Credit: David Prado Perucha – Shutterstock

Whether online, at uni or even on public transport, you've likely come across an ad for private student loans. And one company that keeps popping up is Future Finance.

It's no secret that there are some major issues with how the government's Maintenance Loans are calculated, particularly as they're based on your parents' income.

But, at Save the Student, we're really concerned to see private loan companies trying to profit from this issue by offering students loans that have a much higher interest rate than we think is fair. More worrying still is that the advertising of these loans hasn't always been as transparent as we'd hope (or, if we're honest, expect).

We think that private loans should only ever be used by students as a last resort. If you're considering taking out a loan with Future Finance, or a similar private student loan company, we'd strongly recommend you consider the alternative options outlined below.

Who are Future Finance?

Future Finance Loan Corporation Limited is a for-profit company that offers private loans to students in the UK. These loans come with pretty high interest rates.

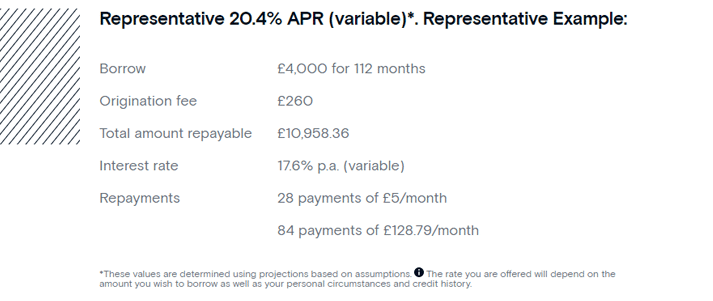

Their website advertises loans of up to £60,000. While their interest rates vary, in October 2022, there was a representative example on their homepage of a £4,000 loan for 112 months at a rate of 20.4% APR (variable). This would result in a sizeable repayment of £10,958.36.

Credit: Future Finance's website

Unlike the government's Student Loans, which you only start to repay when you're earning above a certain amount, the repayment of Future Finance's loans start while you're still at uni. It could potentially increase before you start your graduate job.

During your degree, you'd need to start repaying the loan in reduced monthly amounts. The example loan on their homepage starts at £5 a month, but there's no guarantee it'll be this low for everyone. In fact, it could be anything up to £75 a month while you're still studying.

The average student is already spending around £582 more than they receive in Maintenance Loans each month. It's difficult to see the benefit of taking out a loan at uni if the repayments add to your monthly spending.

Future Finance gives you up to three months after you graduate before charging significantly higher repayment amounts. In the case of the example loan on their site, this would be 84 payments of £128.79.

Unfortunately, not everyone manages to secure and start their graduate job within three months of leaving university. On top of that, it's really difficult to predict this while still at uni. The pressure to start repaying the loan in bigger instalments could add to the already stressful period of graduate job searching.

Save the Student's student money expert, Jake Butler, said:

Every student's situation is different. However, I would suggest that if you're considering taking out a private loan like this, it should be as a last resort.

Borrowing money with such extortionate interest rates can have serious implications and will likely be something you live to regret.

Companies such as Future Finance target students that are desperate by offering what appears to be a quick and easy fix. I would urge any prospective borrowers to look into their alternative options and make the right decision, even if it seems tricky in the short term.

It's a much safer option to start with the official Student Loan from the government. You could also try other alternative funding options first.

Previous controversies with Future Finance

In August 2019, we reported on the news that UCAS had sent an email to students with marketing material about Future Finance. Unsurprisingly, this caused a fair amount of shock and outrage on Twitter.

Among those calling out UCAS for the email were students, the NUS, academics and Save the Student.

In our news piece about the controversy, we looked into past complaints about misleading aspects of Future Finance's marketing. When researching for that article, we were told by the Advertising Standards Authority that they had received five complaints about Future Finance's ads at the time of enquiry in 2019.

Although one was dismissed, the complaints highlighted that their interest rates weren't indicated in adverts and that they'd written 'student loan' in bold. This could have implied they were official Student Loans provided by the government, which isn't the case.

Worryingly, we noticed similar things in the email from UCAS which did not include Future Finance's interest rates. On top of that, it had the phrase 'Wherever you're heading, our flexible Student Loans can help you get there' written in bold.

Particularly when taking out a loan, it's crucial to be as informed as possible to help you make the right choice. Make sure you're fully aware of your options for funding at uni by checking out the alternatives to private loans below.

Alternatives to Future Finance

To avoid private student loan companies, like Future Finance, these are the best alternatives:

-

Student Loan from the government

Credit: Yevgen Kravchenko, kamui29, Bell Photography 423 – Shutterstock

As the first port of call for funding at uni, we'd always recommend the government's official Student Loan.

While the way it's calculated is by no means perfect, the government's Student Loan has a manageable and secure repayment method.

With it, you only repay a percentage of your earnings over a certain amount of money. If your salary ever drops below the threshold, you stop repaying. That way, your monthly repayments should never be anything more than you can afford.

As we mentioned earlier, Future Finance expects you to start repaying the loan they've given you while you're still at uni. After you graduate, you'll have up to three months before the monthly repayment amounts of their loans increase significantly.

Future Finance also say that you can take two three-month breaks from repayments if you're struggling for money after uni. However, the interest would still be added to the loan during these periods.

We know that interest is also added to Student Loans from the government. But, it's a fraction of the percentage added by private student loan companies like Future Finance.

Plus, you only have to repay your government Student Loan for a limited period (depending on whether you're on Plan 1, Plan 2 or Plan 4) before the debt's cancelled. In fact, the majority of people will never repay theirs in full. Future Finance, on the other hand, requires you to pay their loans back in full, with the added interest.

If your Student Loan from the government isn't big enough, we have plenty more funding suggestions below. And, to find out more about your Student Finance options from the government, check out our guide to Student Finance, head to gov.uk or chat to student support at your uni.

-

Extra Student Finance

After getting a Student Loan from the government, there is, unfortunately, a risk that this alone won't be enough to cover all of your living costs.

If this is the case, you can look into extra Student Finance options, like grants, bursaries and scholarships.

There are many different types of funding available, including:

- Scholarships for students from ethnic minority backgrounds

- Disabled Students' Allowances (DSA) which are available to students with mental and physical health problems

- NHS bursaries, including the NHS Bursary, the Learning Support Fund and Social Work Bursaries

- Scholarships for international students.

You may also be surprised by how niche some other scholarships, bursaries and grants are. For example, you could get a grant for being vegetarian, a bursary for having the surname 'Graham' and a scholarship for being talented at e-sports.

-

Family support

Credit: michaeljung – Shutterstock

You may be in a position where your parents are happy and able to support you financially at uni. Getting zero-interest funding from the bank of mum and dad is far less risky than taking out a high-interest private loan.

For a private student loan, you would likely need a guarantor. This is somebody who would agree to make the loan repayments on your behalf if you're unable to keep up with them.

When referring to who can be a guarantor, Future Finance says on their website:

For students, the most common choice is a parent, or another member of their family, such as a sibling, aunt or uncle.

If you were unable to repay your Future Finance loan, your guarantor (likely a parent) would be required to cover the repayments. This, of course, would include interest.

Instead, it's worth seeing if your parents are happy to give you some money so you can avoid a private student loan. In the long run, this could save you and them from having to pay interest on repayments.

To see how much the government expects your parents to give you, check out our parental contributions calculator.

Of course, not all parents can or do give money to their kids at uni.

You could also reach out to other members of your family and close friends to see if they could help you out financially. This might still be as a loan rather than a gift. But, hopefully, it comes with no (or minimal) added interest.

-

Part-time job

Got some spare time at uni between contact hours? Having a part-time job that fits around your studies can make a big difference.

It's one of the most common ways that students fund their living costs, with 56% working part-time. While they're not for everyone, a flexible job can be a great way of making money, while also boosting your CV. Obviously, being able to get a part-time job depends on your degree and uni hours.

For a lot of students, a part-time job involves working shifts in shops, restaurants and pubs. However, there are also a number of other types of jobs you could apply for, too.

If you're looking for ideas, check our list of the best-paid part-time jobs for students.

-

Student overdraft with 0% interest

One of the best perks of having a student bank account is the 0% interest overdraft. This essentially means that you can borrow money from the bank, without having to pay any interest.

If you're in a position where you feel like you need to borrow money to cover uni living costs, we'd urge you to get a fee- and interest-free overdraft from the bank first. Try to get the highest maximum limit possible.

Choosing this route rather than borrowing from private student loan companies (like Future Finance) could work out much cheaper. It gives you an emergency fund to help you get through to your next loan instalment without added interest.

-

Sell unwanted belongings online

Credit: bbernard – Shutterstock

If you're looking for quick ways to make money, see if there's anything you could sell.

Along with the other suggestions on this list, selling your unwanted belongings can help you avoid taking out a private loan.

It's really easy to make money selling things online. It can be anything from old CDs, DVDs and games, to empty toilet rolls.

Your old belongings can be sold on sites like Amazon or eBay. Or, you may want to try upcycling them and selling them on Etsy.

You could also look through your wardrobe for clothes you no longer wear. There are lots of places to sell them – sites like Depop, for example.

-

Student credit cards (repaying the balance every month)

Credit cards should always be used carefully. This means that you should clear the balance before the deadline each month to avoid interest. However, they can really help you get by before the next instalment of your Student Loan.

If you're not confident you'll be able to pay off the balance in time, don't use them. Instead, try getting an extension on your interest-free overdraft. But, when your overdraft is maxed out already, and you're sure you'll be able to repay the money in time, a student credit card can be a good option.

Look out for ones that offer a 0% interest period as an introductory offer. You may need to look beyond student credit cards to find these offers. Please note that it's not guaranteed that your application would be approved.

If you do get a credit card with a 0% interest period, you should be able to make emergency purchases at the end of term without paying any extra interest on top of what you've borrowed.

-

Credit union loans

Tried all of the above and still struggling for money? Before heading to a private student loan company like Future Finance, you could consider taking out a loan from a credit union.

Credit unions are non-profit organisations that are set up by communities. They're intended to help people avoid private loans when they're in need of money.

They generally have much lower interest rates than private loans. That's why it's worth seeing if you can find one that suits you and has reasonable rates first.

If you're unsure where to look, you can head to this website to find credit unions to apply for.

-

Crowdfund your degree

Credit: Pixel-Shot - Shutterstock

This is by no means the easiest suggestion on the list. However, it's still worth considering the option of crowdfunding your degree.

We've heard some great success stories about students who have done this. It'll take some time and effort to set up the best possible online crowdfund page. Plus, you'll need to work hard to get the word out there about your campaign on social media. But, if this method works, it really works.

If you can run a successful crowdfunding campaign for your degree, this not only means you can avoid private student loans, but it would also massively boost your CV. It shows that you have some impressive skills and dedication.

-

Take a year out to save money

We completely get that you might want to crack on with your studies. However, we'd suggest at least having a think about whether a gap year before or during your degree could be worth it.

It might seem like a drastic step, but taking a year out to work and save money can make a massive difference to your finances. If you take the year out instead of borrowing money from lenders like Future Finance, it could save you from making private-loan repayments for years ahead.

There are many options to save money if you take a year out. For example, you could consider finding a full-time job, living with your parents to save on rent and budgeting very carefully.

This is definitely not a decision to rush into. Before deciding whether this is the right step for you, talk to your university about it. They may be able to offer you hardship funds or other support to help you avoid taking a year out. Which brings us to our next point...

-

Discuss your options with university student support

Everyone's personal financial situation is different at uni.

In this guide, we've outlined the best general alternatives to private student loans. But, to ensure you make a decision that's right for you, please also talk to student support services at your university to get tailored advice.

They'll be able to assess your personal situation and suggest the best next steps. It may be that they offer you hardship funds, or highlight which specific grants, scholarships and bursaries you could apply for.

Remember that they're there to help you. You'll never know what support they can offer you until you ask.

Find out the best ways to manage your money and budget effectively at uni with our simple guide.